Promoting Financial Access through Mobile Banking

Banks in United States are in an exciting technological time: The eruption of mobile as a platform for payments and its transformation into a new place of banking services in their customer’s hands. But, what is happening outside of the United States?

There is still a large population in Latin America, which doesn’t have access to financial products. The percentage of households with a deposit account - in a formal financial institution - border around 40% [1] , which brings the question on how banks can increase the number of deposit accounts to the table. There are many approaches and proposals as a possible answer, but the approach I want to propose is based in Mobile Banking.

Mobile, Banking and Commerce: Triggers for the Economical development

There is no magic or rocket science behind the relationship between banking and commerce. This close connection starts to become weaker in the lower social-economical segments: less people have access for deposits accounts and tiny shops use very basic hardware to serve their business. At first glance the gap can be split between a business model design challenge (from the bank perspective) and access to cheap hardware. In this context, I believe a mobile banking solution can help to promote access to financial solutions.

From the perspective of small shops owners, the access to a mobile phone is not a problem at all. In fact the region has a 90% [2] of penetration of this technology, and is still growing. This shows that the problem can be, probably, a business design. Normally I hear complaints from shops owners that banks take a high percentage out of a purchase as a commission fee. However, shop owners do recognize this method is safer than cash, and very easy to handle. Perhaps the problem is a sense of cost and benefit.

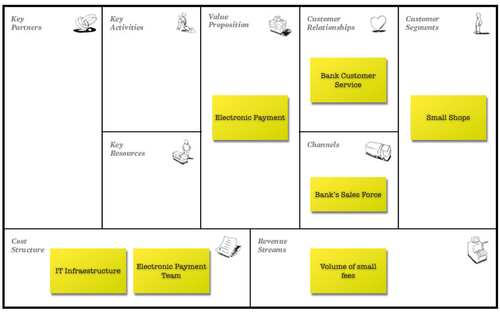

Banks normally say that depending on the amount of transactions, setting up infrastructure to serve this segment can be a positive or negative investment. But if they use mobile solutions to foster the number of shops with point of sales systems (POS) to process electronic payments while offering very low commission rates the possibility exists to find a new revenue stream due the volume of the transactions. We can see this illustrated in the business model design below:

For the users, the main benefit would be access to a non-fee deposit account model, where they can use it to make withdrawals and electronic payments anywhere. Since the tiny shops could implement solutions of mobile payments, they will not need to withdraw money to pay their goods. This could be one of the drivers to incentivize them to deposit money into their account. The main revenue stream for the bank can come from the cross-selling offers as small loans or other instruments as is shown below:

Mobile Banking is not only a platform to promote new ways to serve the banking population, it also can be a driver to promote a new wave of customers in low-income areas for banks. I truly believe the key will be the business model, which is used to implement these solutions.

[1] Financial Access 2010 Report, “The State of Financial Inclusion Through the Crisis”

[2] Latin America enjoys mobile telephone boom

Post image: cc @mauricekoop